Home Loans Made Clear

Whether you’re buying your first home, refinancing, or using your home’s equity, our mortgage team is here to support you from application to closing.

Buying a home can feel overwhelming, but you don’t have to figure it out alone. Whether you’re ready to buy now or still several years away, we’re here to help you understand your options, build confidence, and take the next step when the time is right for you. Especially for first-time buyers, we want the process to feel supportive, clear, and within reach.

“My introduction to Alternatives has been life changing. I’ve accomplished something my mother never accomplished. She never owned any property. She never owned a car. So it’s like a dream come true.”

— Marcus

Start Your Application

Pre-Qualifications, First Mortgages, and Refinances

Buying a home, planning a refinance, or wondering how much house you can afford? Start here. Our online application is the first step toward getting pre-qualified or applying for a mortgage or refinance. Once you submit your information, our mortgage team will review it and guide you through each next step—from document collection to closing—so you always know what to expect. Whether you’re a first-time buyer or a seasoned homeowner, we’re here to make the process smooth and straightforward.

Questions about mortgage/refinance options or application process?

Questions about preparing for homeownership or mortgage-readiness?

Virtual, in-person, phone, and Spanish-language appointments are available

Home Equity Loan & HELOC Applications

Ready to put your home’s equity to work? A Home Equity Loan or Home Equity Line of Credit (HELOC) can help fund home improvements, consolidate debt, cover major expenses, or support life’s big moments. Complete our online application to get started, and a member of our mortgage team will follow up to walk you through your options and help you choose the solution that best fits your needs.

Questions about home equity options or application process?

Virtual, in-person, or phone call available

Our Commitment to Creating Generational Wealth

As a Community Development Financial Institution (CDFI), we work to expand access to homeownership for people and communities too often overlooked by traditional finance. We take a more complete view of every application because homeownership should be more equitable, transparent, and accessible.

Housing Counseling

Preparing for homeownership can bring up a lot of questions, whether you’re ready to buy now or still planning ahead. You can meet with one of our in-house Financial Education Specialists or with a HUD-certified Housing Counselor from our nonprofit partner, BALANCE. Both options offer supportive, one-on-one guidance to help you build a budget, understand your credit, prepare for the mortgage process, and feel more confident about the road ahead.

Downpayment Assistance for First-Time Homebuyers

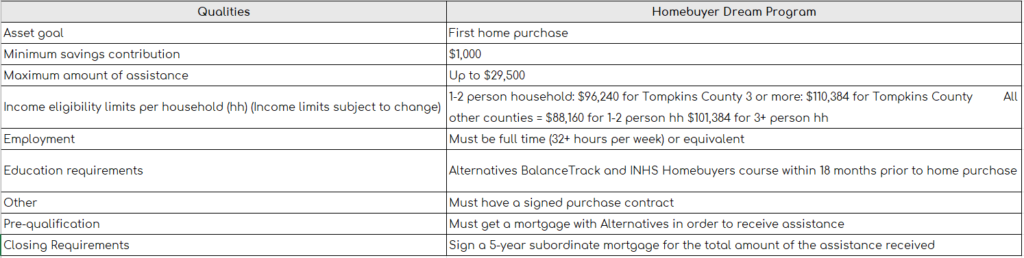

The Homebuyer Dream Program is a down-payment assistance program offered to help low to moderate income first time home buyers in Tompkins, Tioga, Chemung, Steuben, Schuyler, Seneca, Cayuga, Cortland, Monroe, Orleans, Genesee, Livingston, Ontario, Wayne, Yates, Onondaga, and Broome.

This down payment assistance is not able to be counted ahead of time for pre-qualifying. It is recommended that if a household needs down payment assistance to qualify for a mortgage, that they explore options with INHS or other sources of funding.

Once a household has a signed purchase contract and meet all other requirements, they may be eligible to reserve funding. Only after the reservation request is confirmed by the funders, is the household is officially enrolled in the program. The household will then have a total of 120 days to close on the home.

Meeting with Alternatives’ Financial Education staff or mortgage department does not guarantee availability of assistance. Funds are available on a first come, first served basis, and are only reserved for the 120 days after a Reservation Request has been confirmed by the funders.

The household must agree to live in the home for 5 years, otherwise some of the funding may be owed back.

Contact us for more information.

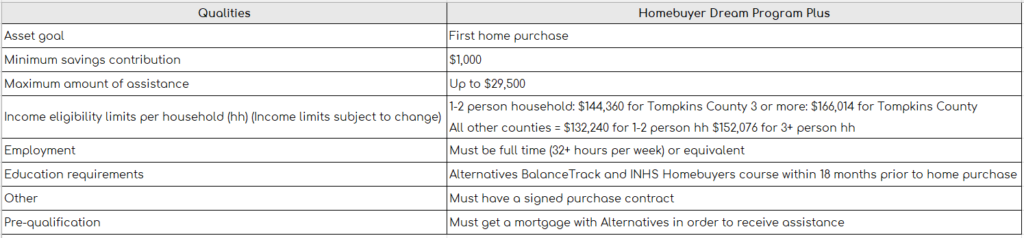

The Homebuyer Dream Program Plus (HDP Plus) is a down-payment assistance program offered to help moderate income first time home buyers in Tompkins, Tioga, Chemung, Steuben, Schuyler, Seneca, Cayuga, Cortland, Monroe, Orleans, Genesee, Livingston, Ontario, Wayne, Yates, Onondaga, and Broome.

This down payment assistance is not able to be counted ahead of time for pre-qualifying. It is recommended that if a household needs down payment assistance to qualify for a mortgage, that they explore options with INHS or other sources of funding.

Once a household has a signed purchase contract and meet all other requirements, they may be eligible to reserve funding. Only after the reservation request is confirmed by the funders, is the household is officially enrolled in the program. The household will then have a total of 120 days to close on the home.

Meeting with Alternatives’ Financial Education staff or mortgage department does not guarantee availability of assistance. Funds are available on a first come, first served basis, and are only reserved for the 120 days after a Reservation Request has been confirmed by the funders.

The household must agree to live in the home for 5 years, otherwise some of the funding may be owed back.

Contact us for more information.

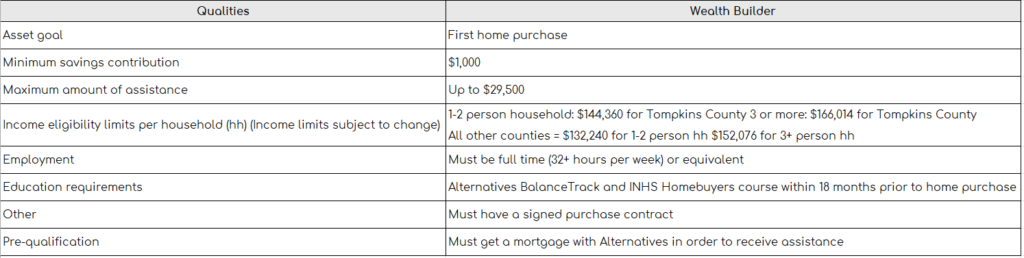

The Wealth Builder program is a down-payment assistance program offered to help low-moderate income first time home buyers who are first generational homebuyers (parents never owned a home). The home being purchased must be located in Tompkins, Tioga, Chemung, Steuben, Schuyler, Seneca, Cayuga, Cortland, Monroe, Orleans, Genesee, Livingston, Ontario, Wayne, Yates, Onondaga, and Broome.

This down payment assistance is not able to be counted ahead of time for pre-qualifying. It is recommended that if a household needs down payment assistance to qualify for a mortgage, that they explore options with INHS or other sources of funding.

Once a household has a signed purchase contract and meet all other requirements, they may be eligible to reserve funding. Only after the reservation request is confirmed by the funders, is the household is officially enrolled in the program. The household will then have a total of 120 days to close on the home.

Meeting with Alternatives’ Financial Education staff or mortgage department does not guarantee availability of assistance. Funds are available on a first come, first served basis, and are only reserved for the 120 days after a Reservation Request has been confirmed by the funders.

The household must agree to live in the home for 5 years, otherwise some of the funding may be owed back.

Contact us for more information.

Have questions about down payment assistance for first-time homebuyers?

Virtual, in-person, phone, and Spanish-language appointments are available

Our Home Loans & Mortgage Programs

Ready to buy a new home or refinance your existing mortgage? Whether you’re upgrading, downsizing, or simply seeking better terms on your mortgage, we’re here to assist.

We’ve designed our home loans to work for everyone – even folks with poor credit or who thought homeownership was out of reach. Our mortgages are more accessible to more people than ever before.

The FAIR Mortgage (Finance Addressing Inequality & Racism) is available to those who make 80% or less of the area median income (AMI) or are first-time, first generation homebuyers making up to 120% of the AMI for the counties we serve.*

This mortgage was designed to break down the barriers to home ownership that many low and moderate income homebuyers and communities of color have historically faced.

This product is for people who are low and moderate income, looking to purchase their first home or refinance within our service area.

Details

-

- No minimum credit score

-

- Borrower’s income must be under 80% AMI (area median income) or less than 120% AMI if they are a first generation homebuyer (parents never owned a home)

-

- Up to 100% loan-to-value with no PMI (private mortgage insurance)

-

- No downpayment required though there will be closing costs (grant funds are available to help cover some of these costs)

-

- More flexible with self employment income (our business development team can help with this)

-

- Competitive Rates

-

- Terms range from 15-40 years

-

- Emergency savings set up automatically at $25 per month

-

- Max $400K loan amount

-

- For primary residences

*Tompkins, Tioga, Cortland, Cayuga, Seneca, Schuyler, Steuben, Chemung, Monroe, Orleans, Genesee, Livingston, Ontario, Wayne, Yates, Onondaga and Broome Counties

Monthly payment example: A mortgage in the amount of $150,000 with an APR of 6.5% would require a monthly repayment including principal and interest back to Alternatives of $948.10 per month. Please note homeowners’ insurance including homeowners’ insurance premiums and/or taxes are not included within this example.

This mortgage product is for purchases and refinances. It allows the option for closing costs to be rolled into the loan. This loan product is not income restricted and may be suitable for borrowers who may not have a lot saved for a down payment and closings costs, but are over income for the FAIR mortgage.

Details

- With 5% down, the borrower can avoid Private Mortgage Insurance

- There is an option to roll in closing costs for an additional amount added on to interest rate

- Term is for 10-30 years, split into 5 year portions. Each 5 years, the rate may adjust

- Each adjustment is up to 2% increase with a lifetime increase of 6% over the starting rate

- The rate will never go below what it started at (floor)

- Max $400k loan amount

- For primary residences

Loan Payment Example: A loan amount of $95,000.00 with an introductory 5% Annual Percentage Rate, (APR), subject to credit score and LTV rate guidelines for a 5/5 ARM( Adjustable Rate Mortgage), principal and interest alone could be as low as $624.00 a month for the first 5 years of the loan, then after the initial fixed 5 year period, rates are subject to adjust yearly thereafter by 2%, but not exceeding 6%. So, for example: the interest rate could be as high as 11% if the introductory rate was starting at 5%, and this would make principal and interest payments as high as $1,019.00. Please note homeowners’ insurance including homeowners’ insurance premiums and/or taxes are not included within this example. Rates are subject to change at any time.

A home equity loan is when you borrow money using the value of your house as a guarantee. Let’s say your house is worth $100,000, and you’ve paid off $20,000 of your mortgage. That means you have $20,000 of equity in your home. With a home equity loan, you can borrow some of that $20,000 if you need it for things like home repairs, school fees, or other big expenses.

Details

- Competitive fixed rates using the equity from your primary residence

- Minimum $10,000, borrow up to $150,000

- 10 or 15-year term

- Borrow up to 90% of the value of your home, minus any outstanding liens

- For a $25,000 loan for a term of 10 years with a 7.00% APR, the monthly payment will be $290.27

- No closing costs if loan is kept open for 3 years

If you have ongoing needs that are better served with revolving credit — but do not want to resort to a credit card — a home equity line of credit (HELOC) may be the affordable answer.

Details

- Competitive interest rates for a wide range of ongoing expenses:

- Home improvements

- Medical expenses

- Renovation projects

- And more

- Direct, any time access to funds

- Revolving credit — when you repay, your limit is replenished for future borrowing

- Affordable payments

- Only pay interest on the part that’s used

- The interest paid may be tax deductible*

- A $25,000 HELOC with a 8.50% APR, the monthly payment will be $246.19 for the first year if all the funds are withdrawn

- For primary residences

- No closing costs if loan is kept open for 3 years

- Minimum $10,000 and borrow up to $200,000 if borrowing 80% or less LTV and borrow up to $100,000 if borrowing 80-90% LTV

*See your tax professional for advice

Questions about buying a home, refinancing, or using your home’s equity?

We’re here to help you understand your options and decide on the next right step.

Virtual, in-person, or phone call available.

Contact our Mortgage Lending Team at Homeloans@alternatives.org.